Bloomberg, reported recently that, “Global demand for corn will come back to the US in the coming months, according to Archer-Daniels-Midland Co., one of the world’s biggest crop traders.

“China recently was buying record amounts of Brazilian corn but with supplies in South America now running thin demand will shift to the US through July when Brazil should start exporting a record safrinha crop. Safrinha is a second-crop corn planted after the soybean harvest.

“‘Of course we lost some bean business but the corn business basically is going to be with us until the crop in Brazil,’ said ADM Chief Executive Officer Juan Luciano. ‘And the US will be exporting a lot of that from here until probably July.‘”

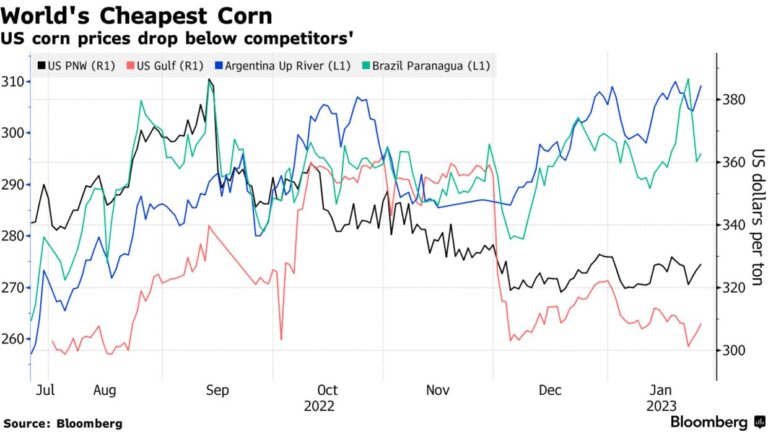

The Bloomberg article noted that, “The pivot could boost corn futures on the Chicago Board of Trade, which are tied to delivery points along the US river system that was battling low water levels and elevated costs. The US traditionally has been the world’s top corn exporter but could lose its crown to Brazil in the coming years.”

The Bloomberg article noted that, “The pivot could boost corn futures on the Chicago Board of Trade, which are tied to delivery points along the US river system that was battling low water levels and elevated costs. The US traditionally has been the world’s top corn exporter but could lose its crown to Brazil in the coming years.”

“Argentina is facing one of the worst droughts in recent years and Brazilian corn exports reached a record 44 million metric tons last year but are starting to trend down as stocks in the country come to an end.”

Also regarding U.S. corn exports, Dow Jones reported recently that, “Export inspections for corn are lower, while marketing year totals continue to drag behind last year’s levels. In its latest grain export inspections report, the U.S. Department of Agriculture said corn export inspections totaled 527,932 metric tons for the week ended January 26. That’s down from 728,792 tons reported last week. The pace of corn export inspections in the 2022/23 marketing year is now even further off from last year’s pace – with inspections this year totaling 12.03 million tons, down over 31% from last year.”

Elsewhere, Reuters reported recently that, “Ukraine has exported almost 26.3 million tonnes of grain so far in the 2022/23 season, down from the 37.9 million tonnes exported by the same stage of the previous season, agriculture ministry data showed recently.

“A major global grain grower and exporter, Ukraine’s grain output is likely to drop to about 51 million tonnes in 2022 from a record 86 million tonnes in 2021,” the Reuters article said.

And a in a separate Reuters article recently, reported that, “Ukraine’s grain harvest is likely to fall to 35 to 40 million tonnes in 2023, including 12-15 million tonnes of wheat and 15-17 million tonnes of corn, a senior analyst and producer said on Monday.”

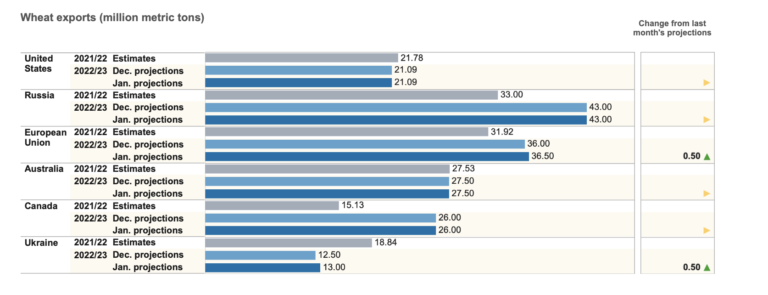

Meanwhile, the USDA’s Foreign Agricultural Service (FAS) indicated in a report last week, “Australia: Grain and Feed Update,” that, “Australia is set for a third consecutive record grain crop, and strong exports. Wheat production is estimated to have reached a record 37 million metric tons (MMT) in marketing year (MY) 2022/23, while barley is estimated to achieve 13.5 MMT of production, the fourth largest on record.”

In more detail regarding exports, the FAS report stated that, “After achieving a second successive year of record wheat exports of 27.5 MMT in MY 2021/22 from 23.8 MMT in MY 2020/21, FAS/Canberra anticipates Australia to achieve a new wheat export record in MY 2022/23 of 28 MMT. This estimate is 500,000 metric tons (MT) higher than the official USDA forecast, largely due to the higher production anticipated by FAS/Canberra for MY 2022/23, the improving grain logistics capabilities in Western Australia, continued strong global import demand and a very strong start to the first two months (October and November 2022) of exports.”

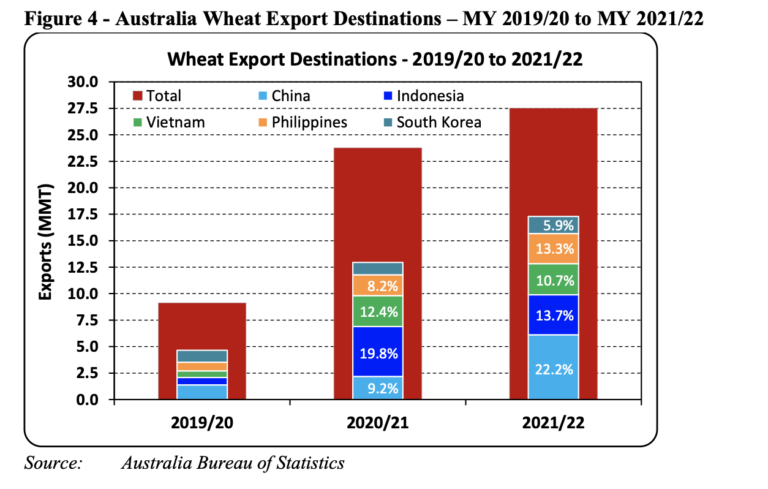

With respect to China, the FAS report indicated that, “For over two decades Indonesia has been Australia’s largest wheat export market by far, but in MY 2021/22 China became the largest destination with 6.1 MMT (22 percent) compared to Indonesia at 3.8 MMT (14 percent).”

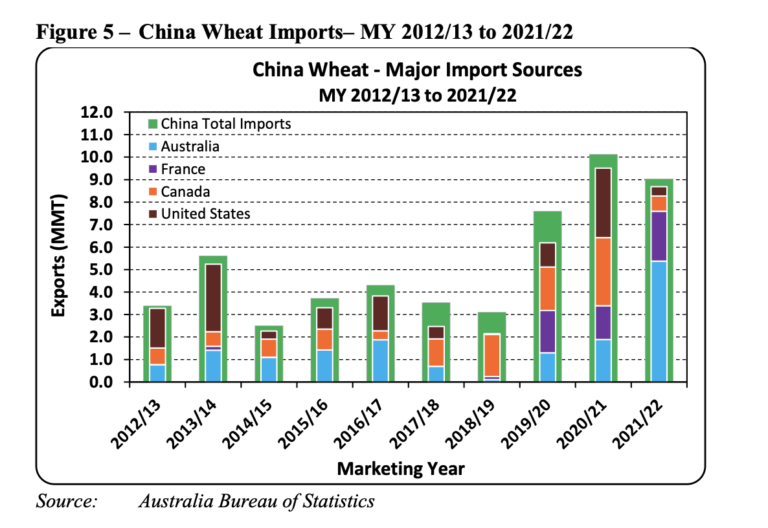

The FAS report added that, “The big increase in China’s imports of Australian wheat have come in conjunction with a large jump in overall wheat imports by China over the past three years. However, for MY 2021/22, with a lack of export supply from Canada in particular after a drought year, China substantially ramped up the volume of imports from Australia to meet its demand.

The FAS report added that, “The big increase in China’s imports of Australian wheat have come in conjunction with a large jump in overall wheat imports by China over the past three years. However, for MY 2021/22, with a lack of export supply from Canada in particular after a drought year, China substantially ramped up the volume of imports from Australia to meet its demand.

For the first two months of MY 2022/23 (October and November 2022) China’s wheat imports from Australia was 652,462 MT, double the volume of the same time in the previous year (324,646 MT).”

In broader news regarding China, Washington Post writers Christian Shepherd and Pei-Lin Wu reported last week that, “Regardless of the veracity of the official pronouncements, many in China now, after a period of caution, appear ready to accept that the pandemic is coming to an end. Holiday train, plane and automobile travel is near pre-covid levels with 700 million trips having been taken as of Jan. 26. Tourists have flocked to popular sightseeing destinations around the country.”

Financial reported recently that, “Chinese growth, at 5.9 per cent, is forecast to be more than double the [IMF’s] October estimate, while India is expected to be the world’s fastest-growing large economy this year, with output 7 per cent higher at the final quarter of 2023 than a year earlier. Together, China and India will account for half of global growth this year, while the US and euro area will account for just 10 per cent, the IMF said.

“China will be an ‘engine‘ that benefits other countries, [Pierre-Olivier Gourinchas, IMF chief economist] said.”

“One big exception to the reopening rally rule is pork, the spot price of which has fallen by almost 50 per cent since Beijing began relaxing Covid restrictions.

“China is the world’s largest producer and consumer of pork, but many homes have switched to cheaper chicken during the pandemic. That has left pig futures traded on the Dalian Commodity Exchange down about a quarter since China began easing restrictions.

“The result, said Darin Friedrichs, a commodity analyst at Shanghai-based Sitonia Consulting, is that China’s contribution to demand for global protein will be ‘weaker than it might’ve otherwise been.

Source: Farm Policy News